Economic and development analysis: Perspectives on economics, society, development, freedom & social justice. Leading issues in Oromo, Oromia, Africa & world affairs. Oromo News. African News. world News. Views. Formerly Oromia Quarterly

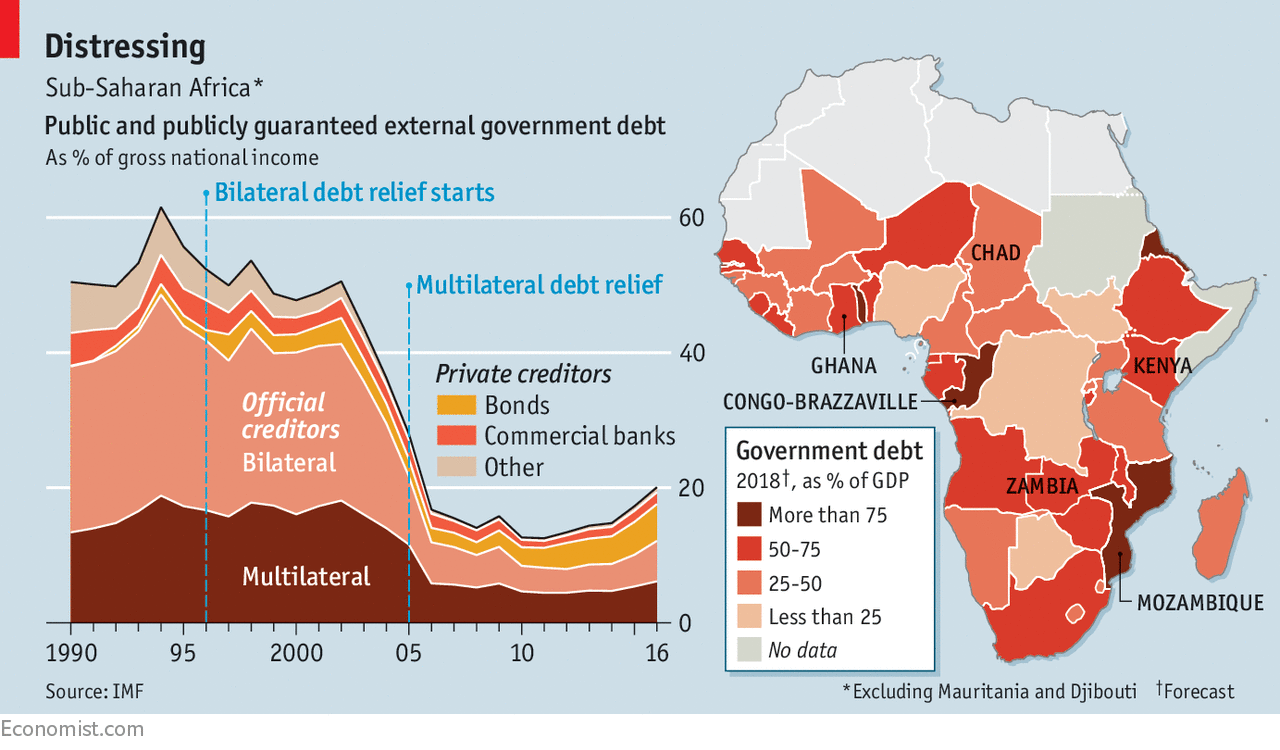

A study of 39 African countries from 1970 to 2010 found that for every dollar borrowed, up to 63 cents left the continent within five years. The money is often siphoned out as private assets, suggests Léonce Ndikumana, one of the researchers, based at the University of Massachusetts, Amherst. Some banks seem more interested in juicy fees than good governance.

China’s involvement in Africa has made it harder to assess the situation. Countries such as Zambia and Congo-Brazzaville have taken out opaque loans from Chinese companies. Angola has borrowed more than $19bn from China since 2004, mostly secured against oil. Such loans often have built-in clauses to review repayments as prices fluctuate, says Deborah Brautigam of the China-Africa Research Initiative at Johns Hopkins University. But there is little precedent for restructuring Chinese loans. Nor is China a full member of the Paris Club, which co-ordinates the actions of creditors when things go wrong.

Though much of the money borrowed by states comes from foreign investors, some is provided by local banks. They find it easier to buy government bills than to assess the reliability of businesses or homebuyers. Moody’s, a ratings agency, estimates that African banks’ exposure to sovereign debt is often 150% of their equity. So a sovereign-debt crisis could fast turn into a banking one.

“A FOOL’S bargain.” That is how Idriss Déby, Chad’s president, now describes the state oil company’s decision to borrow $1.4bn from Glencore, an Anglo-Swiss commodities trader, in 2014. The loan was to be repaid with future sales of crude, then trading above $100 a barrel. But two years later, as the price dived, debt payments were swallowing 85% of Chad’s dwindling oil revenue. For weeks schools have been closed and hospitals paralysed, as workers strike against austerity. On February 21st, after fractious talks, Chad and Glencore agreed to restructure the deal.

Chad’s woes recall an earlier era, when African economies groaned beneath unpayable debts. By the mid-1990s much of the continent was frozen out of the global financial system. The solution, reached in 2005, was for rich countries to forgive the debts that so-called “heavily indebted poor countries”, 30 of which were in Africa, owed to the World Bank, IMF and African Development Bank. With new loans and better policies, many of these countries turned their economies around. By 2012 the median debt level in sub-Saharan Africa (as defined by the IMF) fell to just 30% of GDP. Today the median debt level is over 50% of GDP. That is low by international standards, but interest rates are generally higher for African countries, which collect relatively little tax. Economic growth slowed in response to lower commodity prices. As a consequence, there is much less revenue to service debts. The pace of borrowing has picked up. The IMF reckons that five sub-Saharan African countries are already in “debt distress”, with nine more at high risk of joining them. Lending to Africa surged after the financial crisis, when interest rates in rich countries sank to historic lows. Fund managers chased the high yields of African government bonds and the profits from a commodities boom. The biggest lenders to Africa had long been Western governments. But since 2006, 16 African countries have sold their first dollar-denominated bonds to foreign investors. Interest rates in the rich world remain low, so several countries are scrambling back to the market this year. Senegal’s $2.2bn Eurobond was five times oversubscribed on March 6th. Borrowing makes sense for poor countries if it finances things like roads, schools and hospitals, which improve welfare and support economic growth. But the keenest borrowers in Africa are also feckless spenders. Take Ghana, which racked up debt as it ran an average annual budget deficit of 10% from 2012 to 2016. When a new government entered office last year, it found a $1.6bn “hole” in the budget. The new chairman of the state cocoa board found that a $1.8bn loan meant to fund cocoa production in 2017 was “all gone”.

Ghana got a three-year loan of $918m from the IMF in 2015, ensuring a degree of transparency. Commercial loans are easier to hide. In Mozambique, three state-owned companies borrowed $2bn in deals arranged by European banks. Most of this was done in secret. The proceeds were squandered on overpriced security gear and a bogus fleet of trawlers. An audit could not trace $500m. The once-buoyant economy sank and Mozambique defaulted on its debt last year.

Leveraged corruption

A study of 39 African countries from 1970 to 2010 found that for every dollar borrowed, up to 63 cents left the continent within five years. The money is often siphoned out as private assets, suggests Léonce Ndikumana, one of the researchers, based at the University of Massachusetts, Amherst. Some banks seem more interested in juicy fees than good governance. China’s involvement in Africa has made it harder to assess the situation. Countries such as Zambia and Congo-Brazzaville have taken out opaque loans from Chinese companies. Angola has borrowed more than $19bn from China since 2004, mostly secured against oil. Such loans often have built-in clauses to review repayments as prices fluctuate, says Deborah Brautigam of the China-Africa Research Initiative at Johns Hopkins University. But there is little precedent for restructuring Chinese loans. Nor is China a full member of the Paris Club, which co-ordinates the actions of creditors when things go wrong. Though much of the money borrowed by states comes from foreign investors, some is provided by local banks. They find it easier to buy government bills than to assess the reliability of businesses or homebuyers. Moody’s, a ratings agency, estimates that African banks’ exposure to sovereign debt is often 150% of their equity. So a sovereign-debt crisis could fast turn into a banking one. Disaster can still be averted in most African countries. Abebe Shimeles of the African Development Bank warns against sudden spending cuts, which would leave half-finished infrastructure projects to rust. Research from the IMF suggests that the least costly way to deal with fiscal imbalances in Africa is to raise meagre tax-to-GDP ratios, which have crept up by just a couple of percentage points this century. Other proposals aim to make lenders share more risk with borrowers by, for example, linking interest payments to growth or commodity prices. Some suggest changing laws in America and Britain, where most debt is issued, so that countries are not liable for loans agreed to by leaders acting without due authority. Organisations such as the IMF could be more robust, speaking out early when countries seem to be in a downward debt spiral. As it is, the costs of bad borrowing rarely fall on leaders or their lenders, which often makes politicians borrow (and steal) more. “It’s the common man that actually bears the brunt,” says Bernard Anaba of the Integrated Social Development Centre, a Ghanaian advocacy group. The people of Chad, now paying for Mr Déby’s foolish bargain, would surely agree.- For more click here for The Economist

Related (Oromian Economist Sources):

ECONOMIC COMMENTARY: THE DEBT CHALLENGE TO AFRICAN GROWTH, addisstandard/

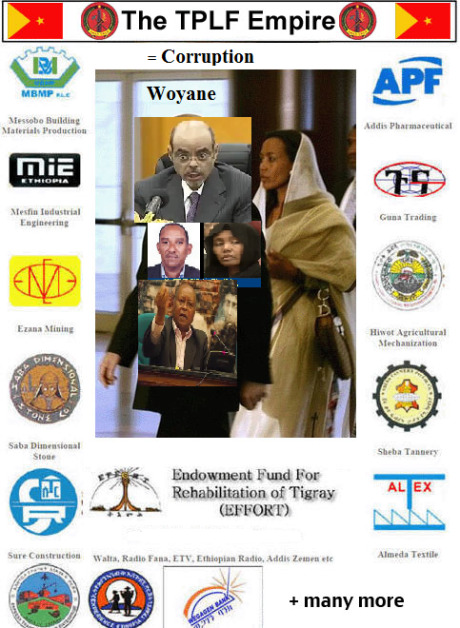

By corroding and weakening governance institutions and the democratic values of human rights, gender equality, justice, and the rule of law, it has hindered the continent’s progress toward peace and prosperity. A 2002 AU study estimated that Africa loses about $150 billion annually to corruption. Illicit financial outflows, particularly in the extractive industry, cost the continent about $50 billion per annum – far exceeding the official development assistance that African countries receive from Organization for Economic Cooperation and Development countries ($27.5 billion in 2016).

An Ethiopian – born business mogul has been named in an anti-corruption crackdown by the Saudi Arabia government over the weekend.

Mohammed Hussein Al Amoudi, 71, was detained along with 11 princes, four current ministers and a number of former ministers. Saudi-owned Al Arabiya television said the probe is headed by Crown Prince Mohammed bin Salman.

Al Amoudi is an Ethiopian – born business man who holds both Saudi and Ethiopian nationality. According to Forbes, as at 2016, his net worth was approximately $10.9 billion.

His investments are linked to oil and global commodities. He is also listed as Ethiopia’s richest man and the second richest Saudi Arabian citizen in the world. He is one of two businessmen detained, the other is one Saleh Kamel.

His two main businesses are Corral Petroleum Holdings and MIDROC. MIDROCdescribes itself as “a global investment group, wholly owned by Mohammed Hussein Al Amoudi.

“It has substantial interests in petroleum, agribusiness, property, industry and industrial services, engineering and construction, tourism and trade and investment, largely in Europe, Africa, the Middle East and North Africa.”

Al Amoudi is said to have migrated from Ethiopia to Saudi Arabia when he was 19 and became a full citizen of the Kingdom in 1965. He built up a private fortune in construction and property before diversifying into the downstream energy sector with major refining and retail investments in both Lebanon and Saudi Arabia.

MIDROC has an international focus with three main operating companies: MIDROC Middle East (based in Saudi Arabia), MIDROC Europe (based in Sweden) and MIDROC Africa where the company’s focus is heavily on Ethiopia. It also has separately managed and significant petroleum interests.

His influence is remarkable. His people are loyal and will not do anything to antagonize him or the regime. If one has close relation to his circles they are guaranteed success. There are many Ethiopians that oppose the regime but will not dare utter a word for fear of alienation.Therefore, the news of his arrest is a huge deal. It is significant event in the history of the region and Ethiopia. This is an event that will quicken the demise of the TPLF as he was a significant player and ardent supporter. Al Amoudi has openly bragged that he is Weyane. But, what is the impact of his arrest and its repercussions? It is the biggest disruption that the TPLF has ever seen.

Sums of money that appear to be linked to corruption cases will be reimbursed to the Saudi state’s General Treasury. (Shutterstock)

Saudi authorities have announced that they will be freezing the bank accounts of suspects detained in the kingdom on corruption charges.

Officials said that there is “no preferential treatment” in the handling of their cases.

The Saudi Center for International Communication, an initiative of the Ministry of Culture and Information, said that sums of money that appear to be linked to corruption cases will be reimbursed to the Saudi state’s General Treasury.

The Saudi anti-corruption committee, which was set up on Saturday by King Salman’s royal decree and chaired by Crown Prince Mohammed bin Salman, had arrested a number of princes and ministers.

More ….

The former Saudi billionaire, Mohammed Hussein al-Amoudi, is under strict security guard in a room on the top floor of one of the most luxurious hotels in the Saudi capital after the Saudi authorities issued a decision to arrest him for his involvement in corruption cases inside and outside Saudi Arabia. And a group of former Saudi businessmen and officials.

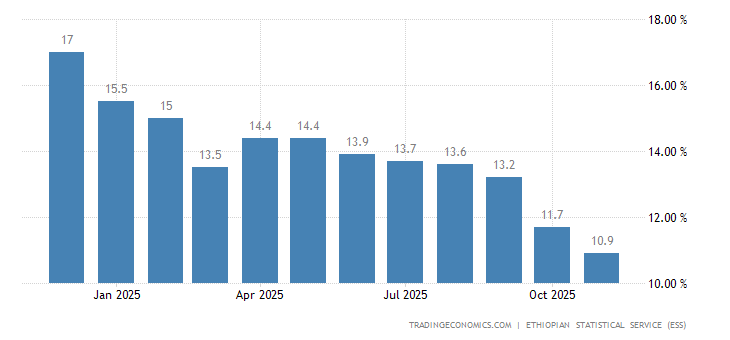

Consumer prices in Ethiopia increased 10.4 percent year-on-year in August of 2017, following a 9.4 percent increase in July. It is the highest inflation rate since October of 2015 as food prices went up 13.3 percent, above 12.5 percent in July and non-food inflation rose to 7.1 percent from 5.9 percent in July. Inflation Rate in Ethiopia averaged 16.37 percent from 2006 until 2017, reaching an all time high of 64.20 percent in July of 2008 and a record low of -4.10 percent in September of 2009.

In Ethiopia, the inflation rate measures a broad rise or fall in prices that consumers pay for a standard basket of goods. This page provides the latest reported value for – Ethiopia Inflation Rate – plus previous releases, historical high and low, short-term forecast and long-term prediction, economic calendar, survey consensus and news. Ethiopia Inflation Rate – actual data, historical chart and calendar of releases – was last updated on September of 2017.

Econometrics – the most practical part of any Economics course. Combining regression analysis with economic theory using real world data sets! This is what applied econometrics is all about!Feel free to download and share my course notes from EC2020 Elements of Econometrics.

Shiller, a behavioral economist, closely tracks investors’ feelings about the market. He believes that emotions can hold the key to market movements. When I saw Shiller late last week for an interview about his new book on the economics of deception (“Phishing for Phools,” written with Fed Chair Janet Yellen’s husband George Akerlof), he told me more investors are worried that the market is over-valued than at any time since the peak of the dotcom bubble in 2000.

“Interest rates have been at zero” for a long time, says Shiller. “The economy has been viewed as sluggish, and yet [corporate] earnings have been growing and prices have been growing at a rapid pace.” That kind of “irrational exuberance,” says Shiller, is exactly what bubbles are made of.

So, why haven’t we seen a major sell-off, one more lasting than the dip we saw a few weeks back, after which the markets quickly rebounded? Because, says Shiller, investors are caught between two dueling narratives about the market.

First, there’s the “New Normal,” story, which is that we’re in a period of low interest rates that will last a long time, and that’s what’s kept markets up. This creates a sense of unease that our recovery isn’t real, but has somehow been genetically modified by central bankers.

“The aggressive monetary policy, which developed as kind of a new approach to managing [the economy] and was largely international, brought us these very low interest rates,” says Shiller. What’s more, “long rates are low, which represents some kind of public attitude that this [new normal] is going to go on for a long time.” As I have written many times, long periods of easy money always create bubbles. Meanwhile, says Shiller, “there’s another not so commonly-raised factor in connection with understanding the market: concern about inequality, which is rising, and also related to that a concern about information technology replacing jobs.”

Both of those things add to the sense that there is bad news lurking underneath those seemingly strong corporate earnings data of the last several years. That makes investors jittery.

But there’s another narrative. America is still the prettiest house on the ugly block that is the global economy. Where else can people park their money, if not in U.S. blue chips? Shiller adds that the growing sense that bad news may be looming can also “encourage people to accept high prices for houses and the stock market because they need to have something for the future.” Rising markets are supported by investors and consumers whoneed them to rise, because it makes them feel richer. “And they’re not going to say, “Oh, this price is too high, I’m going to consume this,” says Shiller. Rather, they accept the higher and higher asset prices – until they don’t anymore. That’s when the bubble bursts.

Those two dueling narratives may be one reason that markets have been volatile of late. People who hold equities have earned a lot of money — the stock market has gone way up. You could conclude, says Shiller, “I’ve got so much money, let’s go on a cruise! Let’s have a lark.” That sentiment drives consumer spending at the higher level. “But maybe you don’t because you’re worried. You have the sense that [things could change] — or maybe you’re worried about your children,” says Shiller. “In 20 or 30 years, I don’t know what they’re going to be doing. I’m just worried. Or maybe they’ll be doing horribly. So let’s keep that stock.” That in turn buoys markets. It’s a somewhat bipolar cycle that fits with the level of volatility we’ve seen all this year, which is much higher than last.

So what happens now? At some point, the market will receive some important new signal. It could be a rate hike from the Fed this week. Or it could be another raft of bad news from China. At that point, we’ll likely see another sell-off. The question then is whether it becomes a stampede. There’s no metric that will answer that question for sure. Emotions, as much as data, hold the key to what the markets will do. No wonder Shiller won the Nobel for saying as much.

In order to facilitate understanding of Soro’s theory, we are interested to reintroduce reflexivity as it is defined and elaborated in Wikipadia as follows:

Reflexivity refers to circular relationships between cause and effect. A reflexive relationship is bidirectional with both the cause and the effect affecting one another in a relationship in which neither can be assigned as causes or effects. In sociology, reflexivity therefore comes to mean an act of self-reference where examination or action “bends back on”, refers to, and affects the entity instigating the action or examination.

To this extent it commonly refers to the capacity of an agent to recognize forces of socialization and alter their place in the social structure. A low level of reflexivity would result in an individual shaped largely by their environment (or “society”). A high level of social reflexivity would be defined by an individual shaping their own norms, tastes, politics, desires, and so on. This is similar to the notion of autonomy. (See also Structure and agency and Social mobility.)

In economics, reflexivity refers to the self-reinforcing effect of market sentiment, whereby rising prices attract buyers whose actions drive prices higher still until the process becomes unsustainable and the same process operates in reverse leading to a catastrophic collapse in prices.

In social theory, reflexivity may occur when theories in a discipline should apply equally forcefully to the discipline itself, for example in the case that the theories of knowledge construction in the field of sociology of scientific knowledgeshould apply equally to knowledge construction by sociology of scientific knowledge practitioners, or when the subject matter of a discipline should apply equally well to the individual practitioners of that discipline, for example when psychological theory should explain the psychological mental processes of psychologists. More broadly, reflexivity is considered to occur when the observations or actions of observers in the social system affect the very situations they are observing, or theory being formulated is disseminated to and affects the behaviour of the individuals or systems the theory is meant to be objectively modelling. Thus for example an anthropologist living in an isolated village may affect the village and the behaviour of its citizens that he or she is studying. The observations are not independent of the participation of the observer.

Reflexivity is, therefore, a methodological issue in the social sciences analogous to the observer effect. Within that part of recent sociology of science that has been called the strong programme, reflexivity is suggested as a methodological norm or principle, meaning that a full theoretical account of the social construction of, say, scientific, religious or ethical knowledge systems, should itself be explainable by the same principles and methods as used for accounting for these other knowledge systems. This points to a general feature of naturalised epistemologies, that such theories of knowledge allow for specific fields of research to elucidate other fields as part of an overall self-reflective process: Any particular field of research occupied with aspects of knowledge processes in general (e.g., history of science, cognitive science, sociology of science, psychology of perception, semiotics, logic, neuroscience) may reflexively study other such fields yielding to an overall improved reflection on the conditions for creating knowledge.

The principle of reflexivity was perhaps first enunciated by the sociologist William Thomas (1923, 1928) as the Thomas theorem: that ‘the situations that men define as true, become true for them.’

Sociologist Robert K. Merton (1948, 1949) built on the Thomas principle to define the notion of a self-fulfilling prophecy: that once a prediction or prophecy is made, actors may accommodate their behaviours and actions so that a statement that would have been false becomes true or, conversely, a statement that would have been true becomes false – as a consequence of the prediction or prophecy being made. The prophecy has a constitutive impact on the outcome or result, changing the outcome from what would otherwise have happened.

Reflexivity was taken up as an issue in science in general by Karl Popper (1957), who called it the ‘Oedipal effect’, and more comprehensively by Nagel[who?] (1961). Reflexivity presents a problem for science because if a prediction can lead to changes in the system that the prediction is made in relation to, it becomes difficult to assess scientific hypotheses by comparing the predictions they entail with the events that actually occur. The problem is even more difficult in the social sciences.

Reflexivity has been taken up as the issue of “reflexive prediction” in economic science by Grunberg and Modigliani (1954) and Herbert A. Simon (1954), has been debated as a major issue in relation to the Lucas Critique, and has been raised as a methodological issue in economic science arising from the issue of reflexivity in the sociology of scientific knowledge (SSK) literature.

Giddens, for example, noted that constitutive reflexivity is possible in any social system, and that this presents a distinct methodological problem for the social sciences. Giddens accentuated this theme with his notion of “reflexive modernity” – the argument that, over time, society is becoming increasingly more self-aware, reflective, and hence reflexive.

Bourdieu argued that the social scientist is inherently laden with biases, and only by becoming reflexively aware of those biases can the social scientists free themselves from them and aspire to the practice of an objective science. For Bourdieu, therefore, reflexivity is part of the solution, not the problem.

Michel Foucault’sThe Order of Things can be said to touch on the issue of Reflexivity. Foucault examines the history of western thought since the Renaissance and argues that each historical epoch (he identifies 3, while proposing a 4th) has an episteme, or “a historical a priori“, that structures and organizes knowledge. Foucault argues that the concept of man emerged in the early 19th century, what he calls the “Age of Man”, with the philosophy of Immanuel Kant. He finishes the book by posing the problem of the age of man and our pursuit of knowledge- where “man is both knowing subject and the object of his own study”; thus, Foucault argues that the social sciences, far from being objective, produce truth in their own mutually exclusive discourses.

In economics

Economic philosopher George Soros, influenced by ideas put forward by his tutor, Karl Popper (1957), has been an active promoter of the relevance of reflexivity to economics, first propounding it publicly in his 1987 book The Alchemy of Finance.[1] He regards his insights into market behaviour from applying the principle as a major factor in the success of his financial career.

Reflexivity is inconsistent with equilibrium theory, which stipulates that markets move towards equilibrium and that non-equilibrium fluctuations are merely random noise that will soon be corrected. In equilibrium theory, prices in the long run at equilibrium reflect the underlying fundamentals, which are unaffected by prices. Reflexivity asserts that prices do in fact influence the fundamentals and that these newly influenced set of fundamentals then proceed to change expectations, thus influencing prices; the process continues in a self-reinforcing pattern. Because the pattern is self-reinforcing, markets tend towards disequilibrium. Sooner or later they reach a point where the sentiment is reversed and negative expectations become self-reinforcing in the downward direction, thereby explaining the familiar pattern of boom and bust cycles [2] An example Soros cites is the procyclical nature of lending, that is, the willingness of banks to ease lending standards for real estate loans when prices are rising, then raising standards when real estate prices are falling, reinforcing the boom and bust cycle.

Soros has often claimed that his grasp of the principle of reflexivity is what has given him his “edge” and that it is the major factor contributing to his successes as a trader. Nevertheless, there is little sign of the principle being accepted in mainstream economic circles.

In anthropology

In anthropology, reflexivity has come to have two distinct meanings, one that refers to the researcher’s awareness of an analytic focus on his or her relationship to the field of study, and the other that attends to the ways that cultural practices involve consciousness and commentary on themselves.

The first sense of reflexivity in anthropology is part of social science’s more general self-critique in the wake of theories by Michel Foucault and others about the relationship of power and knowledge production. Reflexivity about the research process became an important part of the critique of the colonial roots[3] and scientistic methods of anthropology in the “writing cultures”[4] movement associated with James Clifford and George Marcus, as well as many other anthropologists. Rooted in literary criticism and philosophical analysis of the relationship of anthropologist, representations of people in texts, and the people represented, this approach has fundamentally changed ethical and methodological approaches in anthropology. As with the feminist and anti-colonial critiques that provide some of reflexive anthropology’s inspiration, the reflexive understanding of the academic and political power of representations, analysis of the process of “writing culture” has become a necessary part of understanding the situation of the ethnographer in the fieldwork situation. Objectification of people and cultures and analysis of them only as objects of study has been largely rejected in favor of developing more collaborative approaches that respect local people’s values and goals. Nonetheless, many anthropologists have accused the “writing cultures” approach of muddying the scientific aspects of anthropology with too much introspection about fieldwork relationships, and reflexive anthropology have been heavily attacked by more positivist anthropologists.[5] Considerable debate continues in anthropology over the role of postmodernism and reflexivity, but most anthropologists accept the value of the critical perspective, and generally only argue about the relevance of critical models that seem to lead anthropology away from its earlier core foci.[6]

The second kind of reflexivity studied by anthropologists involves varieties of self-reference in which people and cultural practices call attention to themselves.[7] One important origin for this approach is Roman Jakobson in his studies of deixis and the poetic function in language, but the work of Mikhail Bakhtin on carnival has also been important. Within anthropology, Gregory Bateson developed ideas about meta-messages as part of communication, while Clifford Geertz‘s studies of ritual events such as the Balinese cock-fight point to their role as foci for public reflection on the social order. Studies of play and tricksters further expanded ideas about reflexive cultural practices. Reflexivity has been most intensively explored in studies of performance,[8] public events,[9] rituals,[10] and linguistic forms[11] but can be seen any time acts, things, or people are held up and commented upon or otherwise set apart for consideration. In researching cultural practices reflexivity plays important role but because of its complexity and subtlety it often goes under-investigated or involves highly specialized analyses.[12]

One use of studying reflexivity is in connection to authenticity. Cultural traditions are often imagined as perpetuated as stable ideals by uncreative actors. Innovation may or may not change tradition, but since reflexivity is intrinsic to many cultural activities, reflexivity is part of tradition and not inauthentic. The study of reflexivity shows that people have both self-awareness and creativity in culture. They can play with, comment upon, debate, modify, and objectify culture through manipulating many different features in recognized ways. This leads to the metaculture of conventions about managing and reflecting upon culture.[13]

Reflexivity and the status of the social sciences

Flanagan has argued that reflexivity complicates all three of the traditional roles that are typically played by a classical science: explanation, prediction and control. The fact that individuals and social collectivities are capable of self-inquiry and adaptation is a key characteristic of real-world social systems, differentiating the social sciences from the physical sciences. Reflexivity, therefore, raises real issues regarding the extent to which the social sciences may ever be viewed as “hard” sciences analogous to classical physics, and raises questions about the nature of the social sciences.[14]

(NEW YORK) – In recent years, a growing number of African governments have issued Eurobonds, diversifying away from traditional sources of finance such as concessional debt and foreign direct investment. Taking the lead in October 2007, when it issued a $750 million Eurobond with an 8.5% coupon rate, Ghana earned the distinction of being the first Sub-Saharan country – other than South Africa – to issue bonds in 30 years.

This debut Sub-Saharan issue, which was four times oversubscribed, sparked a sovereign borrowing spree in the region. Nine other countries – Gabon, the Democratic Republic of the Congo, Côte d’Ivoire, Senegal, Angola, Nigeria, Namibia, Zambia, and Tanzania – followed suit. By February 2013, these ten African economies had collectively raised $8.1 billion from their maiden sovereign-bond issues, with an average maturity of 11.2 years and an average coupon rate of 6.2%. These countries’ existing foreign debt, by contrast, carried an average interest rate of 1.6% with an average maturity of 28.7 years.

It is no secret that sovereign bonds carry significantly higher borrowing costs than concessional debt does. So why are an increasing number of developing countries resorting to sovereign-bond issues? And why have lenders suddenly found these countries desirable?

With quantitative easing having driven interest rates to record lows, one explanation is that this is just another, more obscure manifestation of investors’ search for yield. Moreover, recent analyses, carried out in conjunction with the establishment of the new BRICS bank, have demonstrated the woeful inadequacy of official assistance and concessional lending for meeting Africa’s infrastructure needs, let alone for achieving the levels of sustained growth needed to reduce poverty significantly.

Moreover, the conditionality and close monitoring typically associated with the multilateral institutions make them less attractive sources of financing. What politician wouldn’t prefer money that gives him more freedom to do what he likes? It will be years before any problems become manifest – and, then, some future politician will have to resolve them.

To the extent that this new lending is based on Africa’s strengthening economic fundamentals, the recent spate of sovereign-bond issues is a welcome sign. But here, as elsewhere, the record of private-sector credit assessments should leave one wary. So, are shortsighted financial markets, working with shortsighted governments, laying the groundwork for the world’s next debt crisis?

The risks will undoubtedly grow if sub-national authorities and private-sector entities gain similar access to the international capital markets, which could result in excessive borrowing. Nigerian commercial banks have already issued international bonds; in Zambia, the power utility, railway operator, and road builder are planning to issue as much as $4.5 billion in international bonds.

Evidence of either irrational exuberance or market expectations of a bailout is already mounting. How else can one explain Zambia’s ability to lock in a rate that was lower than the yield on a Spanish bond issue, even though Spain’s credit rating is four grades higher? Indeed, except for Namibia, all of these Sub-Saharan sovereign-bond issuers have “speculative” credit ratings, putting their issues in the “junk bond” category and signaling significant default risk.

Signs of default stress are already showing. In March 2009 – less than two years after the issue – Congolese bonds were trading for 20 cents on the dollar, pushing the yield to a record high. In January 2011, Côte d’Ivoire became the first country to default on its sovereign debt since Jamaica in January 2010.

In June 2012, Gabon delayed the coupon payment on its $1 billion bond, pending the outcome of a legal dispute, and was on the verge of a default. Should oil and copper prices collapse, Angola, Gabon, Congo, and Zambia may encounter difficulties in servicing their sovereign bonds.

To ensure that their sovereign-bond issues do not turn into a financial disaster, these countries should put in place a sound, forward-looking, and comprehensive debt-management structure. They need not only to invest the proceeds in the right type of high-return projects, but also to ensure that they do not have to borrow further to service their debt.

These countries can perhaps learn from the bitter experience of Detroit, which issued $1.4 billion worth of municipal bonds in 2005 to ward off an impending financial crisis. Since then, the city has continued to borrow, mostly to service its outstanding bonds. In the process, four Wall Street banks that enabled Detroit to issue a total of $3.7 billion in bonds since 2005 have reaped $474 million in underwriting fees, insurance premiums, and swaps.

Understanding the risks of excessive private-sector borrowing, the inadequacy of private lenders’ credit assessments, and the conflicts of interest that are endemic in banks, Sub-Saharan countries should impose constraints on such borrowing, especially when there are significant exchange-rate and maturity mismatches.

Countries contemplating joining the bandwagon of sovereign-bond issuers would do well to learn the lessons of the all-too-frequent debt crises of the past three decades. Matters may become even worse in the future, because so-called “vulture” funds have learned how to take full advantage of countries in distress. Recent court rulings in the United States have given the vultures the upper hand, and may make debt restructuring even more difficult, while enthusiasm for bailouts is clearly waning. The international community may rightly believe that both borrowers and lenders have been forewarned.

There are no easy, risk-free paths to development and prosperity. But borrowing money from international financial markets is a strategy with enormous downside risks, and only limited upside potential – except for the banks, which take their fees up front. Sub-Saharan Africa’s economies, one hopes, will not have to repeat the costly lessons that other developing countries have learned over the past three decades.

The following is the case study on Ethiopia from Opride Contributors http://www.opride.com/oromsis/articles/opride-contributors/3781-sovereign-bond-may-prove-to-be-a-nightmare-for-ethiopia

SOVEREIGN BOND MAY PROVE TO BE A NIGHTMARE FOR ETHIOPIA

By J. Bonsa

Ethiopian has recently joined the sovereign bond market, where governments sell debt to investors with a guarantee that they would pay periodic interest rates and the initial investment value at maturity.The bulk of sovereign bonds are bought by institutions and governments, individual investors constitute a relatively small proportion of total bond buyers. Sovereign bonds are often denominated in local currencies.

Ethiopia’s foray into the sovereign bond market has raised eyebrows in the world of financial market for at least three reasons. First, Ethiopia is the poorest country ever to venture into this market. Second, the real value of Ethiopia’s currency has been deteriorating at alarming rates, devalued by close to 40 percent in the last three years alone. Third, the108-page long prospectus that the Ethiopian government prepared and submitted to formally enter the market contained astonishing revelations. In a bizarre twist, the government made unfamiliar and strange declarations about risks associated with purchasing the bond it is about to issue.

Among other things, authorities warned about: famine, Ethio-Eritrean war, social unrest and upheaval in the aftermath of the May 2015 election. These are extra-ordinary admissions of risks to a scale not heard in this market before. But what is the motive of the Ethiopian government in exhibiting such an extraordinary behavior? What are the triggers for the move to enter the sovereign bond market? In this piece, I will attempt to seek answers to these questions.

Carrot and stick

The local English weekly Addis Fortune reported rumors in Addis Ababa that the unusual admission of the risks was due to naivety of junior staff. However, central government in Ethiopia is known for ordering lower level units to do things a certain way only to deny involvement to avoid blame at a later stage. For example, federal government officials often deny and attribute human rights abuses to local authorities. The latest screw up seems to be an extension of that logic to international diplomacy. The fact that this rumor was leaked through a pro-government newspaper provides further clue about some sinister motives beyond a simple act of incompetence by those who prepared the prospectus.

It is likely that the government used the document as a carrot and stick tactic aimed at Western governments. An evidence of this comes from the revelations about Ethiopia’s “credit lines from China and Chinese entities accounted for 42 per cent of all external loan disbursements in 2013-14, and for 69 percent in 2012-13.” This fact underscores Ethio-Chinese partnerships have been considerably strengthened. Western countries, particularly the U.S., recognize Ethiopia’s support in the global fight against terrorism. But they also know that that support has often been offered to them so officiously with hidden motives, which at times jeopardized Western interests in the Horn of Africa.

The issuance of the sovereign bond and rare admission about the scale of Ethio-China relations appear like a warning to the U.S.: Buy the bond generously if you want to stop us from lurching toward China. The categories of hazards the government chose are even more telling. For instance, the possibility of another war with Eritrea is inserted to gain sympathy and also imply that terrorism is still rampant in Horn of Africa. The likelihood of social unrest after the next election is meant to warn the West that they should not seriously consider pressing the government on human rights and democratization.

Other motivations are rooted in domestic politics. The government knows that the risks are real and investors will find out sooner or later. In that case, by declaring the risks upfront, the regime tries to present itself as a brutally honest and transparent government. In doing so, they might be trying to pre-empt opposition claims about lack of transparency in areas of governance and economic management.

Liquidity crisis

The Ethiopian government has a strange habit of biting more than it could chew. For example, it plans to invest about $5.1 billion per year over the next decade on mega infrastructural projects: power, roads, and telecommunications. Another $6 billion is required to build a 2.4 thousands km railway network. The construction of the Grand Ethiopian Renaissance Dam (GERD) on the Nile River is expected to cost about $4.8 billion. The World Bank has warned that this level of investment (more than 40 percent of GDP and three times the $1.3 billion in infrastructure spending that the country managed during the mid-2000s) is well beyond the country’s modest means.

This created a self-inflicted wound in the form of a very messy liquidity crisis: an acute shortage or drying up of funds in the economy. This crisis is the main trigger for the foray to the sovereign bond market. The shortage of funds is specially manifested in difficulty to borrow funds from the banking system. The crisis has been around in the Ethiopian economy for a good part of the last decade. The government left no stone unturned in the sphere of the domestic economy to overcome the severe liquidity crisis.

But the regime squandered huge sums of free grants and concessionary or low interest loans from donors, annual net-inflows in the upwards of $2 billion, excluding other humanitarian aid.

The debacle from the 2005 election and the 2009 Charities Law, which restricted operations of foreign NGOs, saw a noticeable reduction in foreign aid. The government had to seek non-concessionary loans, particularly from China, to finance its mega projects. Meanwhile, the ill-designed project locations in less productive sectors or regions means sharp declines in export earnings.

For much of the last decade, the government simply printed more and more birr and engaged in a spending spree. However, a limit was reached when inflation hit the roof, approaching 60 percent in 2008. Fearing political backlash through social unrest and also due to pressures from international financial institutions, the government backed down from its inflationary financing strategy.

Involuntary savings

Absent foreign funds, the government maintained a dogged determination and vowed to proceed with the mega projects by entirely relying on domestic savings. This began with sales of government savings bonds to domestic institutions, to raise about $892.2 million in five years. Obviously, this was not realistic. About 70 percent of Ethiopians still live in extreme poverty, and one cannot expect households to voluntarily save even a small proportion of the target amount of saving. Consequently, the government resorted to force savings, using unorthodox methods.

The involuntary savings was accompanied by an intensive propaganda campaign to rally the public around the mega infrastructural projects by creating wartime like atmosphere. It is not only “unpatriotic” to question the suitability or merit of the large projects, it borders with criminality to express any reservations specifically about the GERD. Every civil servant has been forced to buy a saving bond paying her one-month salary in 12 installments. They have also made a relentless but unsuccessful campaign to entice the Ethiopian diaspora. The perverse method applied to sell bonds to households was followed by an even more crude procedures meant to force bonds on the business community. Private Banks have been compelled to purchase bonds equivalent to 27 percent of their annual loans. However, this does not apply to government owned banks. Banking is effectivelygovernment monopoly, the three major state-owned banks hold 73 percent of the total bank assets in the country, 63 percent for the Commercial Bank of Ethiopia alone.

The extent of ignorance among Ethiopia’s policy makers is baffling. The involuntary saving is meant to boost publicinvestment expenditure, which is part of aggregate demand that fuels economic growth. But the authorities grossly overlooked the very act of involuntary saving is bound to reduce the other components of expenditure — household consumption expenditure on goods and services as well asbusiness investment expenditure. Sure enough, the government has belatedly realized there was a limit to achieving their goals through involuntary savings, and with all options in the domestic economy already exhausted.

Sovereign bond

The sovereign bond saga is a yet another maneuver to raise funds the government so desperately needed to finance the ill-conceived mega projects. This time the movement is on a less comfortable and unfamiliar terrain beyond Ethiopia’s borders, in the international market arena where the regime cannot apply brute methods to enforce bond purchases. Perhaps for the first time in its rein, Ethiopia’s ruling party will have to play by the rules.

Accordingly, it set out with a calculated move to secure a “sound” credit rating from known global agencies. In a quick succession during the first half of May 2013, credit rating agencies offered the government exactly what it needed. Fitch Ratings and Moody’s assigned ‘B’ and ‘B1’ ratings to Ethiopia, respectively. These endorsements opened the door for a debut on international capital markets.

However, the government rhetoric notwithstanding, most economic analysts know that the fundamentals of the Ethiopian economy have not reached the level that warranty the kinds of credit ratings offered to Ethiopia. For instance, in May 2012, three months before Meles Zenawi died, theEconomist observed:

JUST how sustainable is Ethiopia’s advance out of poverty? This is a vexed topic among bankers and others in Ethiopia who hold large wads of birr, the oft devalued currency. Despite hard work by the World Bank, oversight from the International Monetary Fund, and studies by economists from donor countries, it is not clear how factual Ethiopia’s economic data are. Life is intolerably expensive for Ethiopians in Addis Ababa, the capital, and its outlying towns. Some think Ethiopia’s inflation figures are fiddled with even more than those in Argentina. Even if the data are deemed usable, the double-digit growth rates predicted by the government of Prime Minister Meles Zenawi look fanciful.

Similarly, soon after Ethiopia received the favorable credit ratings, the International Monetary Fund“warned that the pace of accumulation of public sector debt to finance major investments in dams, factories and housing construction “deserves close attention.”’ Given these reservations about the credibility of Ethiopian authorities, it is perplexing as to why the ratings agencies endorsed Ethiopia to enter the global capital market.

This could have happened only if Ethiopian authorities have utilized their familiar strategy: buying the services of powerful and highly connected lobbying firms. This has become a familiar last resort forauthoritarian regimes in Africa. Ethiopia reportedly allocates a sizeable budget to pay for prohibitively expensive lobbyist service fees.

Public sector debt has been growing at alarming rate. As Horn Affairs reported recently, “Ethiopia’s public sector debt grew threefold in the past five years. The total outstanding external debt surged from $5.6 Billion in 2009/10 to $14 Billion in 2013/14.”These are increasingly becoming commercial or non-concessionary loans such as those from China. Ethiopia’s premature entry into the sovereign bond market amounts to adding fuel to a flame.

IMF predicts Ethiopia’s “total debt to GDP increases from 24 percent to 48 percent of GDP in 5 years, posing risks to debt sustainability. External commercial borrowing entails risks even under the assumption of a highly efficient big-push public investment program.” This means unlike in the past when funds have been flowing in through free grants or soft loans, debt servicing will soon become a huge burden on the Ethiopian economy, given the government’s wasteful investment and a shift from soft to commercial loans. However, it is anybody’s guess whether or not the regime will stay long enough to face the consequences of its decisions.

*The writer, J. Bonsa, is a regular OPride contributor and researcher-based in Asia.

You must be logged in to post a comment.